A sales tax increase from 6.5 cents per dollar to 6.8 cents has been proposed as a way to avoid making deep cuts in important health care investments. The proposal has linked the sales tax increase with a Working Families Tax Rebate, which will refund a portion of the sales tax for lower and moderate income families.

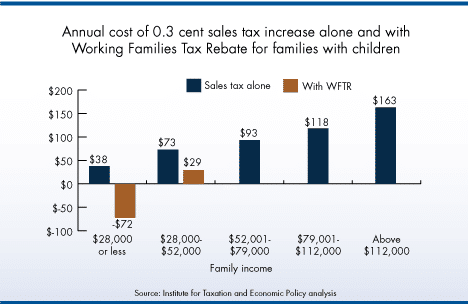

A 0.3 cent increase in the retail sales tax would cost lower income families with kids (those earning $28,000 or less) about $38 annually (see graph below). Upper income families would pay about $163 per year.

While upper income families would pay more in absolute terms, an increase in the sales tax would cost lower income families more as a share of their income. The Working Families Tax Rebate is an important tool for revenue policy because it can offset the impacts of a tax increase for families who are struggling to make ends meet during the recession.

The graph above also shows the net impact of a sales tax increase combined with a Working Families Tax Rebate. Families with kids whose income is $28,000 or less would actually see a net decrease in sales tax. The rebate would also significantly lower the cost of the sales tax increase for the next bracket of earners (those earning between $28,000 and $52,000) so that their total tax increase would be about $29 annually.

Note: Because of the structure of the federal EITC, the Working Families Tax Rebate primarily benefits families with children. Adults without children can qualify for the EITC, but they receive a much smaller credit. The source for these data is the Institute for Taxation and Economic Policy Microsimulation Model.