As we’ve written previously, HB 2201 would make several small, but significant improvements to Washington state’s opaque system of tax breaks. Today’s post focuses on how the bill would fix key flaws in the state business tax return form, which are currently undermining fiscal transparency and accountability by discouraging businesses from accurately reporting their use of state tax breaks.

Policymakers and the public need accurate information about the cost and use of state tax breaks so they can make informed decisions about the future of these tax breaks. However, basic information about business’ use of state tax breaks, such as the specific tax breaks they claim and how much each is worth, is not currently available due to the structure of the current state business tax return.

As a result, the Department of Revenue (DOR) can’t accurately determine the cost of business tax breaks. And, the legislative auditor’s ability to conduct legally-required audits on the effectiveness of state tax breaks is greatly hampered.

The “Multi-Purpose Combined Excise Tax Return,” which businesses use to file and pay their Washington state business and sales taxes, prevents DOR from collecting the high quality information they need about tax breaks in Washington state. Although businesses are legally required to provide details about the various deductions, exemptions, and credits they claim in order to reduce their state tax bills, the tax return is structured in a way that encourages businesses to lump multiple tax breaks into a small number of broad categories instead of reporting detailed information on each tax break claimed. HB 2201 would fix this problem.

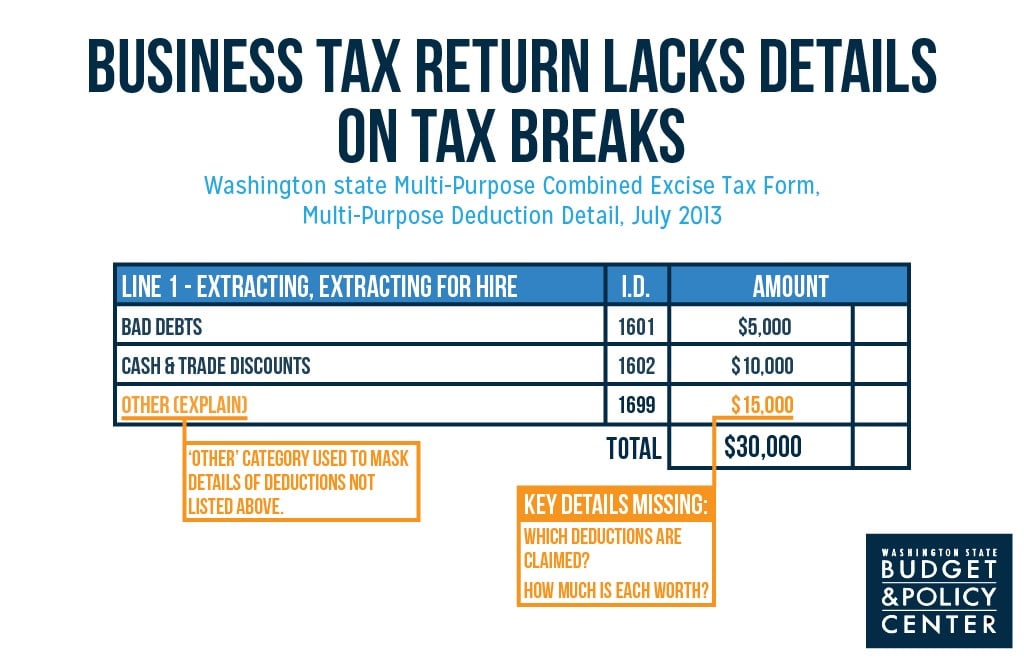

For example, the image below shows a portion of the business tax return that a hypothetical mining company would use to report its business and occupation (B&O) tax deductions. As the figure shows, the company masks the details of $15,000 in deductions by simply categorizing it as “other.”

Too often, businesses do not supply any details about the specific deductions they’ve combined into the “other” category, or other broad categories. In the graphic example, that $15,000 in other deductions could be composed entirely of investment income, which is deductible for non-financial businesses. It also could include $7,500 in investment income and $7,500 in freight costs for ore delivered out-of-state, which is also deductible. There’s just no way to know based on this form.

Without specific line-items for each available deduction, DOR simply cannot collect detailed information about the use of various tax breaks, which, in turn hampers state auditors’ ability to conduct thorough tax break audits. The business tax return also includes overly broad categories for sales tax exemptions.

To fix this problem, HB 2201 would significantly improve quality of information about tax breaks in Washington state by making the following common-sense changes to the business tax filing process:

- Amend the return to require more details about deductions, credits, and exemptions: The Department of Revenue would add separate reporting categories for every B&O and Public Utility Tax (PUT) deduction and credit on the return. Separate categories for all sales tax exemptions would also be added to the return.

- Penalize businesses that don’t report details on business tax deductions and credits: Although businesses are already required to provide details on the various deductions and credits they claim, there is currently no penalty for failing to do so. Under HB 2201 any businesses that fails to accurately report their use of these tax breaks must pay either $50 or 0.5 percent of the value of each unclaimed tax break, whichever is lower.

- Require businesses to report details on sales tax exemptions: Retailers would be required to report specific details about sales exempt from the state sales tax. Businesses that take advantage of certain sales tax exemptions, such as the exemption on manufacturing machinery and equipment, would have to report details of those purchases on their returns.

The bottom line is that the business tax return in Washington state greatly undermines fiscal transparency and accountability. HB 2201 would make reasonable changes that would improve the quality of information about tax breaks in Washington state, allowing the state to pursue a more balanced and holistic state budget.