Last week the Joint Legislative Audit and Review Council (JLARC) presented their recommendations on current tax expenditures to a joint meeting of the House Finance Committee and the Senate Ways and Means Committee. Stick with me, this is important.

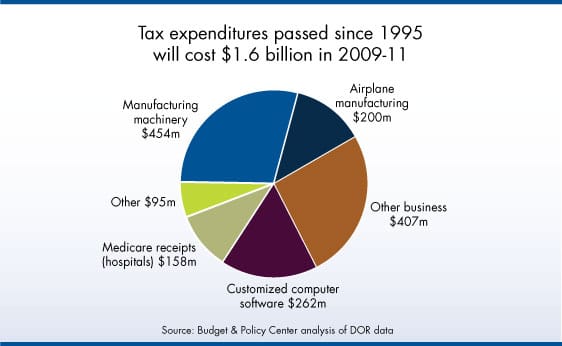

First, what are tax expenditures? They are tax breaks that reduce the funds available for other priorities. In total, we will forego $13 billion of tax revenue in the coming two year budget cycle because of tax exemptions ($1.6 billion from those passed since 1995 alone). Some of these tax expenditures make clear improvements to the tax system. Others need to be reviewed to determine whether they are meeting their stated purpose and whether they are a priority when considered alongside other proposals.

In Washington State, tax expenditures are treated quite differently from other expenditures in the budget process. We regularly review our spending on education, health care, and transportation, but not how to fund tax breaks.

While we don’t do an official biennial review as part of the budget process, in 2006 the Legislature created a process for a long term review. JLARC will conduct intensive reviews of each tax expenditure based on predetermined calendar and make recommendations about continuing or altering most of them (some were excluded from consideration). A Citizen’s Commission for Performance Measurement of Tax Preferences then reviews JLARC’s report and makes independent recommendations to the Legislature.

OK, back to last week. JLARC’s review included 27 tax expenditures ranging from private school tuition to the processing of horticultural products. And they pretty much said to “stay the course” on each of them, with some minor tweaks.

The Citizen’s Commission disagreed in one area. They did not endorse the JLARC recommendation full endorsement the property tax exemption for intangible property (primarily financial assets like stocks and bonds). They had this to say:

Given the magnitude of revenue impact of the exemption ($11 billion in 2008), the dramatic growth of intangible property in the New Economy, and the impact of such a large exemption on the adequacy, efficiency and fairness of the tax system, the Commission recommends that the Legislature study the exemption and consider how to appropriately treat intangible property.*

Is it a good idea to tax intangibles? I don’t know. But the Commission is right that it should be on the table. Further, why not give consideration to tax expenditures every year as part of the budget-making process?

* The Department of Revenue doesn’t think that repealing this exemption would raise that much revenue, in part because it would lower the property tax on tangible property, like houses.